| « Cool Searches in Hoot | Managing Localization in Combo Boxes » |

Education Credits: Beyond the Basics

Note: This article was previously published in Today's CPA, the publication of the Texas Society of Certified Public Accountants. At that time, proposed treasury regulations were not released which change the effect of 1098-T requirements. Buried in the proposed regulations is this reprieve for students who do not receive a 1098-T.

Until the proposed regulations under §§ 1.25A–1(f) and 1.6050S–1(a) are published in the Federal Register as final regulations, a taxpayer (or the taxpayer’s dependent) (other than a non-resident alien) who does not receive a Form 1098–T because its institution is exempt from furnishing a Form 1098–T under current § 1.6050S–1(a)(2) may claim an education tax credit under section 25A(a) if the taxpayer (1) is otherwise qualified, (2) can demonstrate that the taxpayer (or the taxpayer’s dependent) was enrolled at an eligible educational institution, and (3) can substantiate the payment of qualified tuition and related expenses.

Also not mentioned in that article are the new due diligence requirements. Effective in 2017 paid preparers claiming the American Opportunity Tax Credit are required to answer the questions in the AOTC column on Form 8867.

Tax incentives for education may be the most overlooked and most abused items on an individual tax return. They are frequently criticized for their complexity, with each form of education credit or deduction having different rules. With some credits as easy targets for fraud some practitioners are leery of education credit claims. Other problems with these incentives are not so obvious. Software support is limited and taxpayers are not always aware of the benefits or may have false notions about the requirements.

This article focuses on the American Opportunity Tax Credit (AOTC) with incidental mentions of the Lifetime Learning Credit (LLC) and other benefits. It then goes beyond the frequently published basic requirements with a look at IRS regulations that enhance the credits.

The AOTC is an expansion of the Hope Credit, which was created by the Taxpayer Relief Act of 1997, along with the Lifetime Learning Credit. The credits are governed chiefly by IRC § 25A.

Taxpayer Qualifications

In general taxpayers can receive a credit for qualifying educational expenses paid during a tax year. The credit is equal to 100% of the first $2,000, and 25% of the next $2,000, with 40% of the total credit refundable. It is phased out between $80,000 ($160,000 joint) and $90,000 MAGI ($180,000 joint). Also, the taxpayer must not file married filing separately.

The taxpayer must be claiming a dependency exemption for the student which can be any dependent for which the taxpayer is allowed to take a dependency exemption, including individuals that meet the test for dependency exemption as a qualifying relative.[1] So, it’s possible to claim the credit for a student who is a parent or a person whom the taxpayer supports and who lives with him all year.

The taxpayer must not be claimed by someone else as a dependent. One of the quirks in this requirement is that dependency and the dependency exemption amount are separate issues.[2] Clarifying the exemption amount Chief Counsel Advice in 2002 determined that a taxpayer who could have been claimed as a dependent could have a zero exemption amount and claim the credit if nobody claims the exemption.[3]

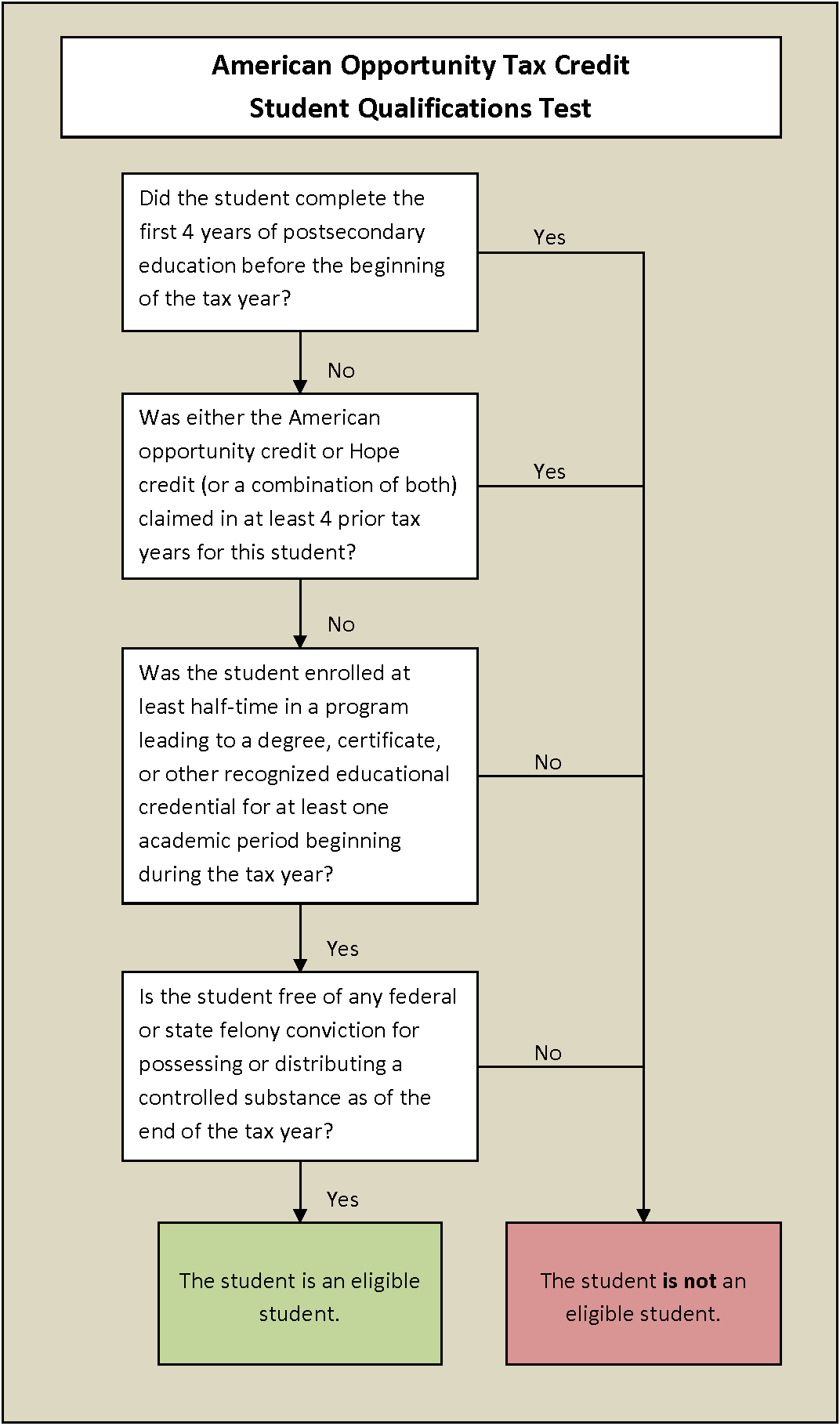

Student Qualifications

Generally, once dependency is determined, the rest of the qualifications relate to the student and the expenses used to claim the credit.

- Student must be pursuing an undergraduate degree or other recognized education credential

- Student must be enrolled at least half time for at least one academic period beginning during the year

- No felony drug conviction on student’s record

- Available for first 4 years of post secondary education

- Cannot be claimed more than 4 tax years

Qualifying Expenses

Expenses that can be used to claim the credits include costs of tuition and required fees, as well as required books and course materials. When available the 1098-T can provide the amount of qualifying expenses for the AOTC though preparers should verify the amounts reported. A 1098-T is not always provided.

Currently books and other course materials have to be required, but they do not have to be purchased at the institution to qualify. If an institution or degree program requires the student to have a computer it may also be considered a qualifying expense. Expenses unrelated to the educational program are not qualifying expenses.[4] Non-qualifying expenses include

- Room and board

- Insurance

- Medical Expenses (including student health fees)

- Transportation (including parking fees)

- Living expenses

Qualifying Payments

In addition to having qualifying expenses, the taxpayer must have made payments for those expenses in the tax year. Payments for qualifying expenses include amounts paid by the student, the taxpayer, or through student loans. Special rules apply to certain qualified installment agreements which could affect the recognition of payments.[5]

Payments made by a third party may also qualify as paid by the taxpayer if paid directly to the institution. In that case, the taxpayer is treated as receiving the payment from the third party and, in turn, paying the qualified tuition and related expenses.” [6] So if a grandparent pays the institution for part of the cost of attending college, the taxpayer can claim the credit using those amounts. Those payments (tuition only) are also exclusions from the gift tax and without regard to relationship.[7] Also considered paid by the taxpayer are amounts paid by certain scholarships that the student includes in income.

Generally payments must be made in the year the term begins. Payments made for educational expenses for the first three months of the following year can also be considered as qualifying in the year paid. Qualifying expenses are also limited to amounts for attendance at an eligible educational institution. The institution must be an eligible to participate in Title IV programs such as Pell grants and federally insured student loans.[8]

It is important to be familiar with all the nuances of 1098-T reporting and verify its accuracy. For example, although 1098-T may indicate graduate student status, the requirement is that the student has not earned a four-year degree, but that test is made based on the beginning of the tax year, not the end of the tax year. If a student graduated in May, all expenses for the year still qualify for the AOTC. In fact, prepaying for the first semester of graduate school in the next year is also an option.

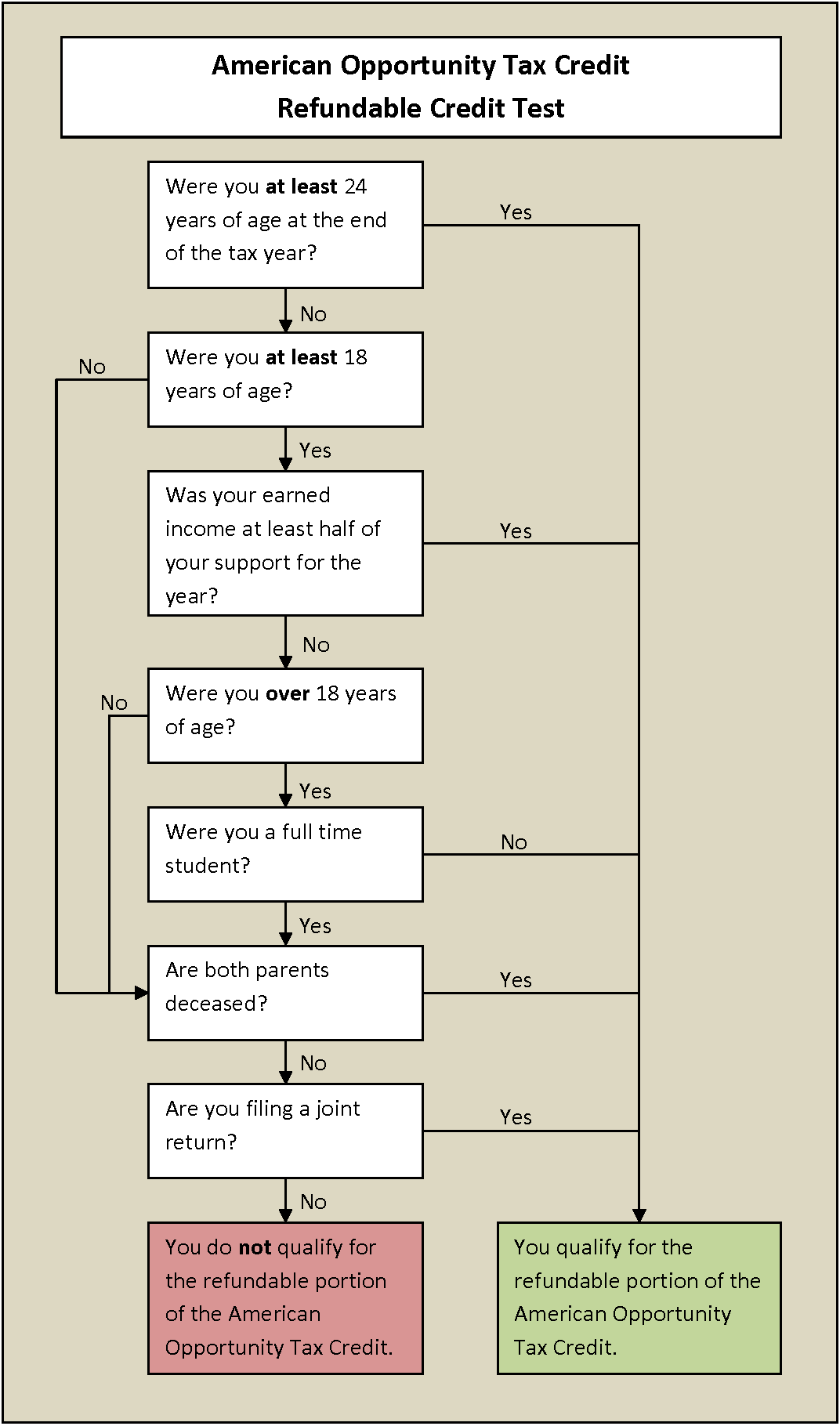

Refundable Qualifications

Additional qualifications exist for the refundable portion of the credit. Students age 24 and over qualify for the refundable portion of the credit, as well as parents of children under the age of 24 if they claim the child as a dependent.

Publication 970 lists those who do not qualify for the refundable credit but it may be easier to reverse the logic to see which taxpayers do qualify. While many students under the age of 24 do not qualify for the refundable portion of the credit, it is important to review the regulations that apply to each case as there are several exceptions.

The Refundable Credit Test flowchart can help in evaluating whether the refundable qualifications are met. Publication 970 already has a flowchart to identify eligible students for the AOTC.

Lifetime Learning Credit

The LLC is not as generous as the AOTC but it does not have as stringent student qualifications. While it must be for attendance at an eligible educational institution, it does not require the student to be seeking a degree credential. The expenses can be used to pay for expenses to simply help the student acquire or improve a job skill. The LLC does not require half-time attendance and isn’t limited by a drug felony conviction.

Up to $10,000 of expenses can be considered in calculating the 20% credit for a maximum credit of $2,000, and the taxpayer can take the credit for an unlimited number of years. Qualifying expenses for the LLC include costs of tuition and required fees, as well as required books. Books DO have to be required and purchased at the institution to be qualified expenses for the LLC.

Whether the taxpayer uses the LLC or decides to use a tuition deduction may depend on his income and marginal tax rate. The credit is phased out for modified MAGI between $52,000 ($104,000 joint), and $62,000 ($124,000 joint).

General Scholarship Treatment

For both the AOTC and LLC, scholarships are often treated as tax-free when applied to qualified expenses, in which case the qualified expenses for the credits are reduced by that amount. The tax code defines the term qualified scholarship as any amount used for qualifying expenses and refers to both scholarships and grants.[9]

Scholarships (or fellowships) that are paid for services rendered to the institution, such as teaching or research, are not qualified scholarships and should be reported to the taxpayer on a W-2 and included in income. There are some exceptions to this requirement.[10]

Scholarship Inclusion

While scholarships generally offset expenses, the regulations do allow taxpayers to treat some scholarships differently in order to increase their qualifying expenses. Treas. Reg. § 1.25A-5 enhances/clarifies the options taxpayers have when claiming education credits and gives the procedure for calculating expenses for the credit.

Three Types of Scholarships

Although not defined as such in the code, scholarships can be defined as exclusive, taxable, or elective based on the terms of the scholarship. Exclusive scholarships are those scholarships, by the terms of scholarship, which must be used exclusively to pay qualified expenses. The full amount of the scholarships must reduce the amount of qualified expenses and are tax-free up to the amount of those expenses.

A taxable scholarship is one that must be used exclusively for other than qualified expenses, or is taxable for other reasons. Room and board is not a qualifying expense, so scholarships that cover only that is normally taxable. Scholarships in excess of qualifying expenses are also taxable.

Elective Scholarships

The third type of scholarship is the elective scholarship. If any amount of a scholarship “may or must be used” for other than qualified expenses the taxpayer can elect to treat it as tax-free and offset qualified expenses or include it in income. When treated as income, the amount of qualified expenses is not reduced and the taxpayer may qualify for a higher education credit.

Scholarships that are available for elective treatment include Pell grants. Most other federal aid, as well as Coverdell Educational Savings Accounts and Qualified Tuition Plans (Section 529) can also be effectively treated as elective scholarships.[11]

If a scholarship covers both specific qualified and non-qualified expenses such as tuition or room and board, the taxpayer can choose how to allocate the amounts, but may be limited by the amount of actual expenses. If the scholarship is $6,000 and room and board is $5,000, $5,000 is the most that can be applied to non-qualified expenses.

Measured Scholarships

There is no regulation that addresses scholarships that are measured by the amount of tuition, as opposed to must be used for tuition, but IRS rulings do support the elective nature of such scholarships. In 1999 the Louisiana legislature went from a system that required a TOPS award to be used for tuition to a system that measures the amount of the award by the amount of tuition. That change in the wording was the defining characteristic that allowed scholarship inclusion in the Louisiana TOPS program. In the IRS private letter ruling (PLR) related to the Louisiana Tuition Opportunity Program for Students (TOPS) program in Louisiana, it was determined that the TOPS awards could be used for either qualifying or non-qualifying expenses and the exclusion of the grant was determined by the tax reporting of the taxpayer.[12]

Following the ruling, the Louisiana Law Review published an article encouraging recipients of the TOPS grant to amend their returns to claim prior year education credits.[13] The terms of the Texas Grant now contains similar wording and although PLRs cannot be used as precedent, the same reasoning can be used to consider that as elective in the same manner.

The focus of scholarship inclusion is often on the AOTC, but elective scholarships can be treated the same way in calculating the LLC. The LLC is not refundable so the benefit is limited to the amount of tax owed. Scholarship inclusion will also incur an increase in tax at the taxpayer’s tax bracket while only generating a 20% credit.

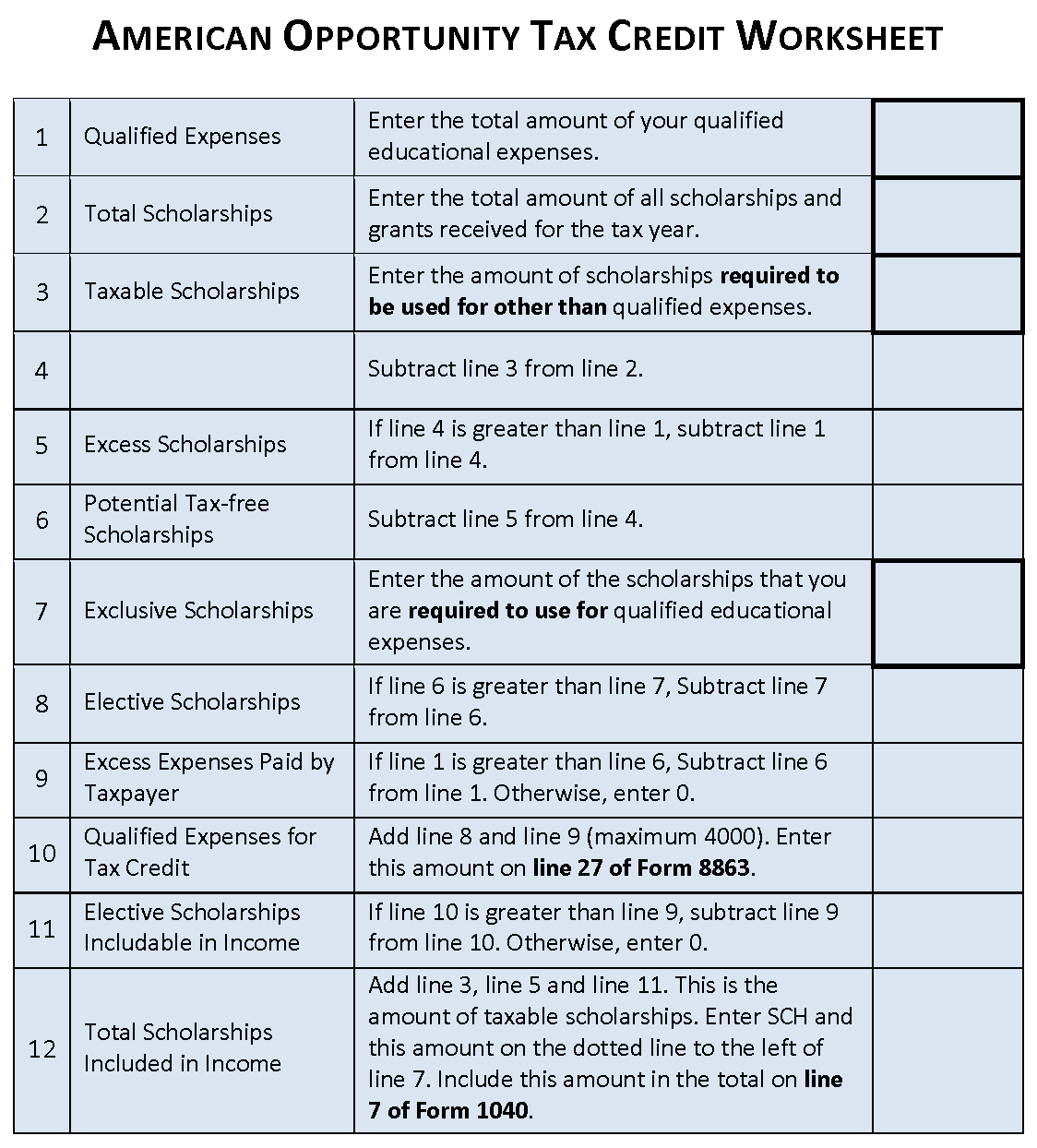

Scholarship Calculations

The IRS provides several examples of adjusting qualifying expenses using scholarship inclusion in Treas. Reg. § 1.25A-5 and Publication 970. For instance, in two examples in Publication 970 the taxpayer includes $4,000 of his Pell grant in income in order to claim that amount for the AOTC.[14]

One of the problems with calculating education credits is that software doesn’t handle the calculations when scholarship inclusion is involved or when coordinating benefits. Where only scholarships are considered, the AOTC worksheet provided here can calculate the maximum credit amount, by adjusting qualifying expenses to equal the maximum $4,000.

Coordinating With Other Benefits

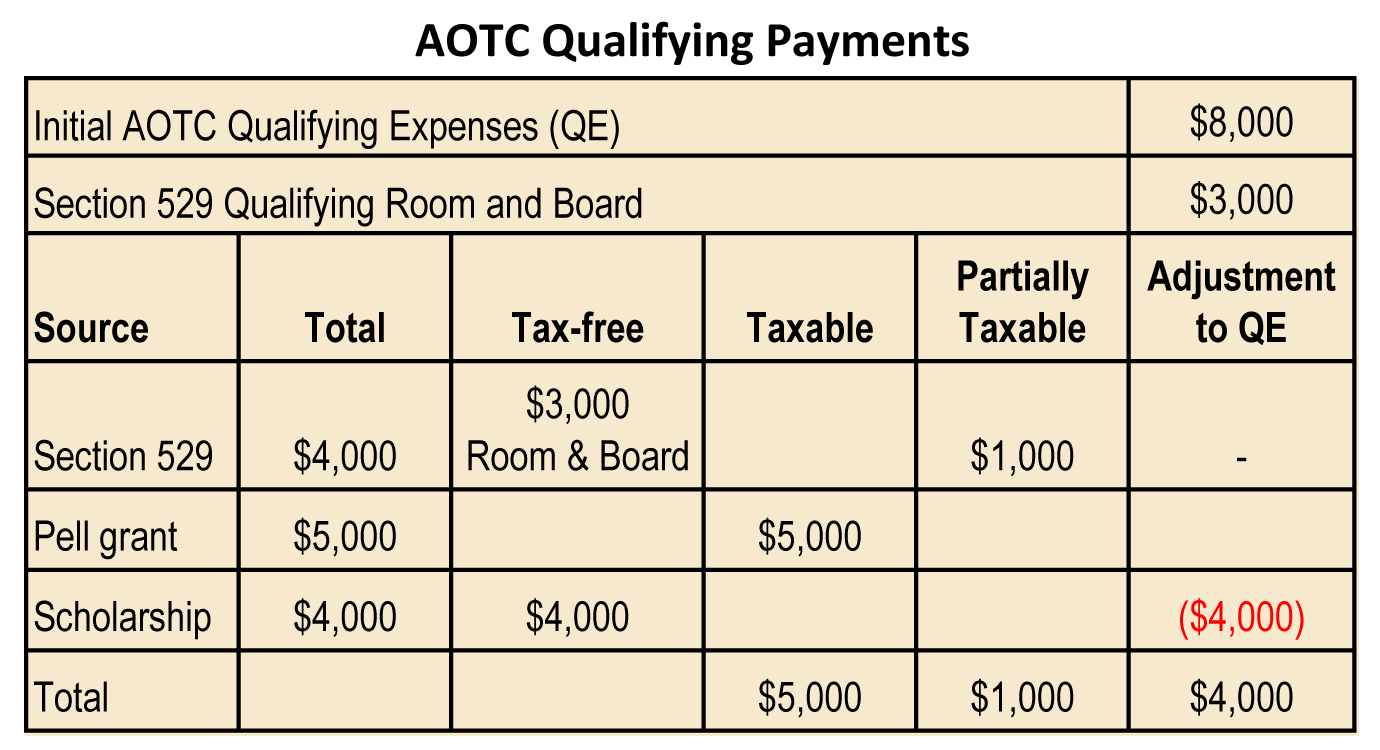

Just as taxpayers can coordinate their credit with scholarships, they can coordinate with other educational benefits with different qualifications. For example, room and board is a qualifying expense for Section 529, but not for AOTC. By systematically considering each benefit and making adjustments to qualifying expenses, it is possible to determine the best claiming strategy. Consider the following example:

Taxpayer has AGI of $48,000 and is claiming AOTC for a dependent child. AOTC qualifying expenses (QE) were $8,000, and room and board was $3,000. He received $4,000 from a Section 529 account. The student also took a $5,000 student loan. After acceptance, he received a $5,000 Pell grant and a $4,000 scholarship that was required to be used for tuition, fees, and room and board. Because his scholarships and grants exceeded his qualifying expenses, he did not receive a 1098-T.

The first step is to allocate $3,000 of the Section 529 to cover room and board (tax-free). Next the $4,000 scholarship can be allocated to tuition and fees, reducing QE to $4,000. Instead of using the Pell grant to offset the remaining expenses, the student can include that $5,000 in income and the taxpayer can claim AOTC on the remaining $4,000 of expenses paid. The taxable portion of the remaining $1,000 of Section 529 is also taxable to the beneficiary, pro-rated based on earnings.

The scholarship is not used for room and board because it is not tax-free for that purpose. Section 529 was not used to cover part of the tuition because it is only partially taxable. No penalty applies to the Section 529 distribution because both the scholarships and qualified expenses were more than the distribution amount.[15]

IRAs for Education

IRA distributions can also be used for educational expenses without incurring a penalty and they do not have to be for education expenses when taken. If an IRA distribution was for home improvement and later in the tax year the taxpayer incurs education expenses, the amounts can be allocated to the education. Unlike Section 529, amounts are taxable and the amount qualifying for penalty exclusion is reduced by other payments for qualified expenses. In the above example, if an IRA distribution was used instead of Section 529, the $1,000 would also be subject to the 10% penalty. With Roth IRAs, distributions up to the amount of contributions are tax-free.

Family Coordination

One of the quirks of education credits involves coordinating returns of the taxpayer and student. If the taxpayer claims an education credit based on including scholarships in income, it is the student, not the taxpayer, who must include the scholarship in income. Paid expenses can be used by whoever claims the credit but scholarships are always the student's responsibility.

The challenge is that the student may be increasing his taxable income, while the parent is enjoying the credit. In order to avoid family conflict it is possible to file Form 8888 to allocate part of the refund to the student by depositing an amount in her bank account that offsets the student’s sacrifice.

One factor to consider when only the refundable credit is being claimed is the credit percentage. The refundable credit can be viewed as 40% of the first $2,000 and 10% (40% * 25%) of the next $2,000. This 10% is important when student must include taxable scholarships in income and tax is owed on it. With the minimum tax rate at 10% the credit from the second $2,000 is wiped out by the scholarships being taxed.

Education Tax Update

Education was addressed Congress on two occasions during in 2015. In June the Trade Preferences Extension Act of 2015 added a provision requiring taxpayers to have a 1098-T payee statement to claim an education credit.[16] The law is effective for tax years beginning after enactment, i.e. the 2016 calendar tax year.

Then in December, with the passage of the Protecting Americans from Tax Hikes (PATH) Act of 2015, the AOTC was made permanent and due diligence requirements were added. That law also enhances Section 529 benefits with the most notable change being that expenses for computer equipment, software, and Internet access are now tax-free if used primarily by the beneficiary.[17] Since Coverdell rules refer to this code section, computers will also be tax-free expenses. Section 529 account rules were also changed to eliminate the distribution aggregation requirements, and account owners can now avoid penalties due to tuition refunds by contributing the amount back to a 529 account within 60 days of the date of the refund.

The IRS is also addressing the regulations in light of the legislation requiring a 1098-T. Because current regulations allow institutions to forego sending the 1098-T to many students, some taxpayers may not be able to claim the credit they would otherwise have qualified for. Proposed regulations[18] will address that discrepancy by requiring institutions to send 1098-T to most students. Comments are being received until October 31 and a public hearing is not scheduled until November 30, so changes may not be final until into 2017. In the interim, the regulations provide the following reprieve:

Until the proposed regulations under §§ 1.25A–1(f) and 1.6050S–1(a) are published in the Federal Register as final regulations, a taxpayer (or the taxpayer’s dependent) (other than a non-resident alien) who does not receive a Form 1098–T because its institution is exempt from furnishing a Form 1098–T under current § 1.6050S–1(a)(2) may claim an education tax credit under section 25A(a) if the taxpayer (1) is otherwise qualified, (2) can demonstrate that the taxpayer (or the taxpayer’s dependent) was enrolled at an eligible educational institution, and (3) can substantiate the payment of qualified tuition and related expenses.

Education Tax Planning

The many incentives available make education tax planning a complex area but the benefits available allow prudent taxpayers to save on ever-increasing education expenses for themselves, children, and grandchildren. An education saving and spending plan is almost as important as a retirement plan. In both cases, it is important to consider all of the options available and the consequences (or benefits) of distributions, credits, exclusions, and deductions throughout the process.

About the Author:

Dana Bell, EA – Tyler, Texas – is author of the book Education Tax Credits: And Other Educational Incentives.

[1] IRC § 25A(f)(1)(A)(iii)

[2] IRC § 151(d)(2) and Treas. Reg. § 1.25A-1(f)

[3] PLR 200236001 <http://www.irs.gov/pub/irs-wd/0236001.pdf>

[4] Treas. Reg. § 1.25A-2(d)(3)

[5] Treas. Reg. § 1.25A-5(e)(4)

[6] Treas. Reg. § 1.25A-5(b)(2)

[7] Treas. Reg. § 25.2503-6(b)(1)(i)

[8] 20 USC § 1088(b)

[9] IRC § 117(b)(1)

[10] IRC § 117(c) and (d)

[11] IRC § 530(d)(2)(C)

[12] PLR 200137006 <http://www.irs.gov/pub/irs-wd/0137006.pdf>

[13] Kalinka, Susan. "TOPS Scholarship Recipients Who Failed to Claim the Education Tax Credits for 1998 Should Consider Filing Amended Returns." Louisiana Law Review 60.1 (1999): 281-91. <http://digitalcommons.law.lsu.edu/cgi/viewcontent.cgi?article=5806&context=lalrev>.

[14] https://www.irs.gov/publications/p970/ch02.html#en_US_2014_publink1000300227

[15] IRC § 530(d)(4)(B)(iii) and (v)

[16] IRC § 25A(g)(8)

[17] IRC § 529(e)(3)(A)(iii)

![]() This entry was posted on January 18th, 2017 at 01:28:00 pm by Dana Bell and is filed under Professional, Tax Accounting, Today's CPA.

This entry was posted on January 18th, 2017 at 01:28:00 pm by Dana Bell and is filed under Professional, Tax Accounting, Today's CPA.